With the July 30th MPC meeting approaching, Pakistan’s 11% policy rate against 3.2% inflation creates a punitive 7.8% real interest rate—nearly double India’s 3.4% and over five times China’s 1.4%

Pakistani businesses pay double regional financing costs while facing electricity at 12-14 cents/kWh versus 5-9 cents regionally. Meanwhile, unemployment sits at 22% compared to India’s 4.2% and China’s 4.57%.

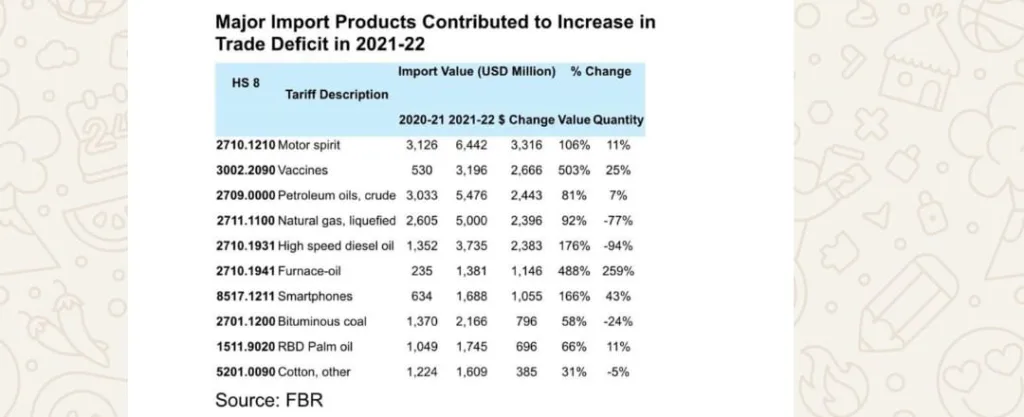

The 2022 boom-bust cycle with $17.5 billion current account deficit was not caused by low interest rates but by $3 billion vaccine imports and $12 billion in higher oil and gas payments due to Ukraine war-induced global energy price spikes—factors completely unrelated to domestic interest rates.

FBR targets 18% revenue increase while monetary policy suppresses the business activity generating taxes. State Bank reserves rose $5.4 billion to reach $14.46 billion (as of 18th July 2025) through borrowing—not exports or productive growth.

Cut policy rate to 9% immediately and to 6% by 31st December 2025.

This aligns Pakistan’s costs with competitors, enables expansion, creates jobs, and reduces debt servicing by PKR 3 trillion annually.

Pakistan has the manufacturing capacity and export potential—only restrictive monetary policy blocks realization of this economic strength.

July 30th determines whether businesses receive competitive support or continued systematic disadvantage.

Pakistani industry demands monetary leadership that prioritizes productive enterprise.

In Economic Policy there are many tools to kerb Consumer Goods and Excessive imports to protect from Boom and Bust cycles . Paying Rs 3 Trillion Higher in Domestic Debt Servicing by keeping 11% policy Rate which is 6 % Higher than Full year inflation of 5 % is not Justified