As part of continuing efforts to improve its communications with external stakeholders and to bring more transparency to monetary policy decision-making, the State Bank of Pakistan (SBP) released its bi-annual Monetary Policy Report (MPR) today. The report reviews macroeconomic developments and outlook that guided the Monetary Policy Committee’s (MPC) decisions since the publication of the August 2025 MPR.

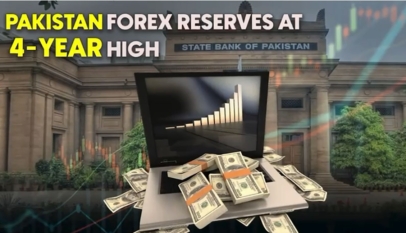

The report noted that macroeconomic conditions and the outlook have improved, supported by a prudent monetary policy stance and continued fiscal consolidation. Inflation is projected to remain within the 5 – 7 percent target range during most of FY26 and FY27, despite some near-term volatility. The current account deficit is projected to remain contained at 0 – 1 percent of GDP in FY26, with a higher trade deficit partly expected to be offset by robust workers’ remittances and planned official inflows. As a result, SBP’s FX reserves are expected to rise to $18 billion by June 2026 and increase further in FY27, reaching close to 3-months of import cover. Economic activity has also strengthened, amidst ongoing macroeconomic stabilization, ease in financial conditions, and the recent reduction in the Cash Reserve Requirement to 5 percent. Accordingly, economic growth prospects have improved, and real GDP growth is now projected in the range of 3.75 – 4.75 percent for FY26, and growth is expected to increase further in FY27.

The MPR also underscored evolving risks to the macroeconomic outlook. While risk of widespread impact from the recent floods have receded, uncertainty from global tariff-related developments persists, alongside volatility in global commodity prices. Domestically, challenges from below-target revenue collection and impact of potential adverse climate events remain sources of vulnerability for the outlooks of inflation, external account and GDP growth. In this context, it is important to speed up the progress on structural reforms to increase the economy’s resilience to adverse shocks, and to improve productivity and plug losses of state-owned enterprises.

The MPR also features four box items that discuss key macroeconomic concepts related to monetary policy. One box provides an update about the monetary policy transmission mechanism in light of the sizable earlier reduction in the policy rate from June 2024 onwards and the transmission lag of 6 – 8 quarters. Another box explains the use of heat maps as an alternative tool for gauging the level of economic activity by consolidating signals from multiple indicators across different sectors into a single visual summary. The next two boxes discuss the important role of surveys and structured interactions of the SBP with other important economic stakeholders, especially in the private sector, to supplement the data-oriented conduct of monetary policy.